Venture Debt — the route of royalty

If you’re aware of dramatised entrepreneurial shows in the US, this might ring a bell.

“I’ll offer you the $275k, but I want an 8 % royalty per unit until I’ve doubled my money”

It’s the words uttered by Kevin O’Leary, a Canadian multi-million dollar entrepreneur and Angel, who over the past decade has garnered popularity as Mr Wonderful on Shark Tank. And as you could expect, what has caught the eye of many avid viewers like myself, has been his somewhat romanticised affair with Royalty deals - which according to the CNN comprise c.35% of his on-air portfolio to date; materially higher than any other investor on the show.

The concept of Royalty originally had its roots in the mineral mining sector during the the mid 1900’s. Companies faced a lack of options to sufficiently fund their operations and capital expansion initiatives. Thus Investors begun to pile up on NPI royalty (Net profits interest) which delivered upfront capital in exchange for a fixed % of future mineral profits. Whilst the concept grew in commercialisation during the 1980’s, it wasn’t until the last decade that it emerged as a popular financing alternative for technology companies- right about when Shark Tank hit the air…

So it’s fair to say that not all entrepreneurs on the show bite and as we’ve discovered, perhaps because of its lighter track record in comparison to more traditional and well used priced offers.

With all that said, you’re probably expecting me to hit you with “ So what is Royalty Financing, and is it a better route to take as a founder or investor? Instead, I’m going to illustrate this for using the above example — one that is based on a real offer aired on the show in 2019.

But in any case, heres a quick synopsis:

Royalty-based financing or Revenue Based Financing (RBF) provides an alternative to raising capital through traditional cash-for-equity ,one thats routinely transacted across early-stage venture . Investors here, exchange capital for a fixed % of future revenue until the specified principal is paid in full. The maturity as well as royalty rates/return cap will vary subject to the term sheet.

Distilling the RBF Proposition

To get a better grasp of the RBF model, let’s begin with a fictitious B2B E-Commerce business called Muffler, an online rental marketplace. With a capital raise on the cards, it’s looking to onboard its first strategic investor alongside fresh capital to help offset an early cash trough.

Let’s now ground some simple assumptions.

- Ask : 275k

- Exisiting Cap Table: Founder (100%)

Muffler

- Forecast Period : 7 years

- Volume (Year 0) : 100,000

- ASP (Year 0) : $25

- Net-profit margin : 30%

I’ve constructed a simple model below to illustrate Muffler’s profile over a 7-year forecast period:

Now with this in mind, there are two offers to consider with their respective deal terms laid out below. Both are offering the $275k ask.

- Mr Wonderful

- Hybrid deal : 5% equity + 8% royalty/sale until double the principal is recouped ( 550k).

- Implies a post-money val. ~ $5.5m

Footnote : Deals are rarely structured per/sale alike Mr Wonderful’s and more commonly tied up with monthly recurring revenue or MRR

2. Investor B

- 20% straight equity

- Implies a post-money val. ~$1.375m

Footnote (“What’s Post-money val.”) : 275K / 5% = $5.5m, 275k/20%=$1.375m

At first glance you wouldn’t jump at either offer, or would you?

Founders, humans and Australians are all naturally subject to the primacy effect and this is what makes the proposition difficult to assess. It’s a cognitive bias illustrating the tendency of people to recall the first piece of information they face. E.g If I were to ask you what the beginning scene of the Lion King was and the scene exactly half way through, I’d 99.9% of the time expect to hear the former and not the latter. If we look at both deals, the first deal boasts 4x the post-money val of the second and opening an offer with this inference in mind is certainly not easy to shake off - especially for a first- time founder.

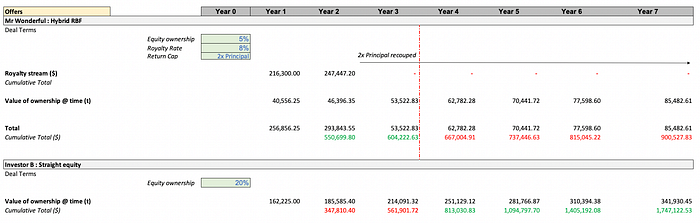

Mr Wonderful’s RBF proposition would thus be better understood by breaking down both deals side-by-side and forecasting the next ~5.5m in sales (Assuming Year 0 follows the round close).

I’ve developed a model below, again conscious of the many assumptions that have been mindlessly grounded into the pro-forma.

There’s a lot going on here, so let me walk you through it:

Return Cap

- We’re first assumed a royalty rate of 8%, which means for every unit sold, the investor receives 8% of the ASP; which would be 8% * $25= $2 @ Year 0.

- However, the RBF stream ends when Mr Wonderful recoups double the principal investment, which by simple calculation is $275k * 2 = 550K. This is the return cap.

- We can see from the above that by Year 2 , double the principal is paid-back ( $550.7k) by Muffler . Hence from then onwards, the RBF stream terminates and Mr Wonderful is left with 5% straight equity in perpetuity.

Vested Interests

By nature, unlocking the benefits of RBF boils down to the efforts of both the founder and Investor. Its this shared alignment towards growth, which sets it apart from other more common deal structures such as cash-for-equity, SAFE’s or convertibles. The investor is incentivised to place the business in its best position to sell, driving down customer-acquisition costs (CAC) and boosting brand awareness. In other words:

“ The more you sell, the more I make”

This is all well and good … until the return cap is met.

Up until year 3, the cumulative value of Mr Wonderful’s investment clearly edges that of Investor B and it’s largely due to his front- end inflow of royalty across Years 0–2. However when this terminates, Mr Wonderful is left with his initial 5% in perpetuity with an exit not likely anytime soon. By Year 4, Investor B’s cumulative ownership emerges the higher of the two.

Therefore the inevitable silver-lining to the RBF model, is rooted in not only the alignment of both parties, but more so their vested interests. Peter Thiel, arguably one of the most polarising figures in Venture Capital to date, is an avid believer in this concept. He quotes:

“ Equity is a powerful tool… Anyone who prefers owning a part of your company to being paid in cash, reveals a preference for the long term and a commitment to increasing your company’s value in the future.”

Having any degree of equity in a business, is an allocation of onus both now and into the future. The more equity, the greater “seat” you have as an advisor in the future trajectory of a business. It is then no surprise to see Mr Wonderful’s value plateau by year four, given there is no expectation of hyper-growth or a large equity exit plan beyond his front-end efforts. With an exit needed to capitalise on the investment, Investor B’s interests are far the contrary and incentivised to unlock the rewards of longer-term alignment.

Now neither offer is a sure-fire bet, let’s make that clear. But like all bets, where your investment stands in 1 year, 10 years or 20 years time lies in the hands of a probability distribution. I’ve laid out one of an infinite basket of possible scenarios Muffler could realise and even then, who is to say which is the “better proposition” for either parties - asking an investor and founder the same question would likely yield very different answers.

So here is my two cents on the matter. Angel investing is exactly the opposite to any speech your former school principal, Ted-X prodigy or inspirational TikTok has ever addressed you with.

“ Its about the destination, not the journey”

Regardless of the route of financing , as long as the business returns an annualised IRR ≥ 50% and 5000x return at exit - I wouldn’t think there’d be many complaints to be made . Whether you’re a founder or investor, you’re here to make money and RBF is certainly one way to do that, a little faster and without the fuss of equity.

State of venture debt in Australia.

Beyond dramatised reality TV, RBF is practiced globally and is becoming more routine in early-stage tech , especially by firms outside the US. In 2010, the year after Shark Tank was aired , five firms were founded and by 2019 more than 30 emerged.

This has seen more than $2.1bn of capital deployed to date (TechCrunch), but what % of this has come from our Aussie ecosystem?

Founded in 2020, Melbourne-based fund Tractor Ventures is one of the few home-grown RBF financiers that have gained recent traction in Australia. The fund commonly issues loans at a~4x return cap in exchange for~5% share of monthly revenue until the multiple is paid off. Since launch it has realised average growth of 130% MoM (Startmate). Only a month ago, another Melbourne revenue-based investment firm Fundsquire , raised c.$75m from investment firm Fasanara Capital with intentions to launch new products across the UK, US and Australia. The team have realised a 2x MoC over the past twelve months and it’s clear the tailwinds are picking up ever so slowly. Firms such as Lighter Capital (Seattle, US) have too taken the step, last-year partnering with NAB to launch their offering in Australia.

Yet amongst the crowd, Clearco is the firm making current headlines with former Dragon on Canada’s Dragons Den, Michelle Romanow, bringing her business to Aussie shores. The firm unlike the previously mentioned, are E-commerce focused with already c.US$2.5 billion deployed into more than 5000 businesses in the US, UK and Canada. So a) Why E-Commerce b) Why Australia?

a) E-Commerce businesses like Muffler in the example I used, simply put are a perfect candidate for RBF financiers. Whilst they might not have a desire to be hyper-growth, their ability to generate cash flow in a predictive manner with more measured and leaner operations makes them suitable. SaaS (Software-as-a-service) businesses too, fit this criteria and arguably even better so.

b) Australia is harbouring one of the largest E-Commerce markets globally, and its expected to hit $45bn by 2025 (Antler). For Aussies in their early 20’s there are two things that constitute 80% of your existence:

- Social Media

- Buying stuff

If this doesn’t fit you, then you must be an outlier - but as we know from High-school statistics class. Outliers are irrelevant.

In any case, these two components are the current driving force behind the immense growth in E-Commerce. The rise of the Creator Economy has meant Aussie social media users are getting younger and younger, whilst E-Commerce giants like THE ICONIC , continue to deliver almost 2 million parcels/day nationwide and set the tone for incumbents. There is certainly a shift in the breed of startups emerging out of Australia, with COVID-led pivots to off-premise systems and online domains making it open-season for E-Commerce & SaaS startups. Australia is seeing an inflexion point in early-stage investment and RBF is certainly ready to bite.

Whilst it wont ever come close to displacing equity financing, Revenue-Based Financing is an alternative Aussie founders should heavily consider, no matter how stubborn you are and especially if you’re not looking to go to the moon.

After all, things do look better from a distance.